In today’s rapidly evolving insurance landscape, an array of disruptions — including rising prices, new risks, and competitive entrants to the market — has sent ripples through the industry, compelling incumbent insurers to reassess their strategies for sustainable growth.

Amid these challenges and disruptions, a resilient and adaptable insurance core system emerges as the linchpin to secure insurers’ growth and innovation. Insurance core systems should not be seen as static entities, but as dynamic enablers for expansion across states, products, and more. Rather than merely maintaining legacy systems, insurers must enhance them to accommodate continuous advancements and customer-centric solutions.

In this blog post, we’ll delve into the current disruptions affecting the insurance industry and introduce an approach that insurers can employ to drive core innovation so they can tackle these challenges effectively.

Navigating Insurance Disruptions with Core Innovation

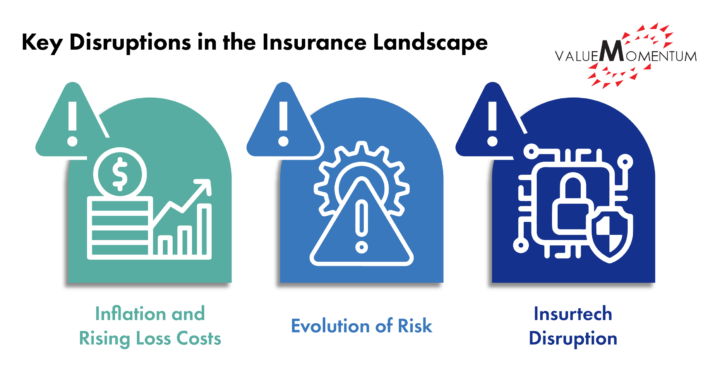

The insurance industry has not been safe from an increasingly unpredictable world. Insurers struggle to differentiate themselves amidst new competitors and the need for specialized coverages, all while dealing with the increasing frequency and severity of weather events, inflation, rising reinsurance rates, and more. The insurance landscape is marked by several key disruptions:

- Inflation and Rising Loss Costs: Inflation is driving up loss costs across markets, posing a challenge to underwriting profitability and exerting additional strain on the revenue side. More customers will reevaluate their insurance coverage and elect to assume more risk to cut expenses. Escalating loss costs and reserve demands have a detrimental impact on profitability. One way to accommodate this loss will require insurers to assess which risks — especially those of specialty — to provide coverage for and differentiate beyond prices. Insurers will need advanced underwriting capabilities to adjust pricing models that account for rising costs and inflation scenarios.

- Evolution of Risk: Changing risk dynamics, driven by factors like natural catastrophes and cyber risks, demand a reevaluation of insurance products. This has caused reinsurance rates to rise and diminish coverage options, which are further contributing to market hardening and rising operational expenses for primary insurance carriers. Despite the pessimistic outlook, commercial insurance providers have a substantial chance to proactively address the expanding protection gaps by centering innovation and product offerings to cover such new risk exposures.

- Insurtech Disruption: The rise of insurtechs and non-traditional insurers is altering market dynamics. Their strong advantages over digital channels and strategic partnerships are reshaping the market landscape, increasing policy options, and reducing entry barriers. While some insurers benefit from insurtech solutions in areas like underwriting and claims, established insurers face competition from these customer-focused companies, which are reshaping customer expectations. To thrive, insurers must invest in core innovation, including modernized digital capabilities that utilize their historic data for enhanced customer segmentation and product innovation.

The Core Conundrum: Balancing Maintenance and Growth

Most insurers are aware of these challenges and are taking measures to build the necessary capacity for core innovation to both offset and transcend these disruptions. Despite this knowledge, a substantial portion of insurers’ investments in their core systems is allocated to “keeping the lights on,” or maintaining existing operations. According to Datos Insights (formerly Aite-Novarica Group), more than 50% of core budgets from both large and midsize insurers is spent on the “run” of core systems.

This approach, while essential, can become a roadblock to innovation if it doesn’t strike a balance between maintaining the current state and fostering future growth. The traditional separation of initiatives into “run” and “grow” categories can hinder the integration of these essential functions and limit the focus on technical operations versus the accomplishment of larger business outcomes. This compartmentalization often results in fragmented technology stacks and limits the potential for sustained business growth.

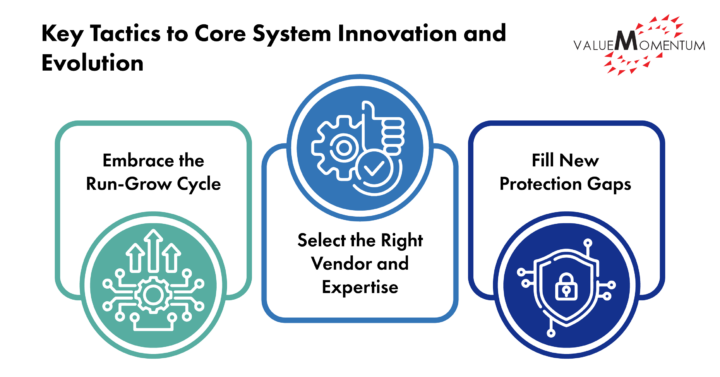

To overcome these challenges, insurers need to bundle “run” and “grow” in their approach to core system innovation and evolution. A few key tactics can serve as a guide:

- Embrace the Run-Grow Cycle: Shifting from a linear perspective of “run” and “grow” to a relational cycle can be transformative. Run and grow are not isolated phases but rather intertwined processes that feed into each other. Insurers must envision a continuous loop where the enhancement of core functionalities leads to growth opportunities and growth triggers further advancements in the core.

- Select the Right Vendor and Expertise: Choosing a vendor with expertise across the entire spectrum — run, grow, and transform — can be a game changer. A strategic vendor partnership ensures a seamless transition across all stages of the insurance life cycle. From implementing new technologies to ongoing maintenance and expansion, a knowledgeable partner can drive consistent growth while keeping disruptions at bay. More importantly, insurers need a partnership that can significantly streamline the “run” of core systems to free up both IT budget and talent and focus on the “grow.”

- Fill New Protection Gaps: With this trifecta of run-grow-transform in mind, innovation can begin by identifying emerging risk protection gaps. Insurers need to explore how their core systems can evolve to address these new risks effectively. Whether it’s developing coverage for intangible assets like cryptocurrency or providing solutions for net-zero transition risks, core innovation should be guided by a deep understanding of the evolving risk landscape and a value proposition ready to address emerging risks.

The Path Forward: Core Innovation for Sustainable Growth

The transformation of the insurance industry hinges on insurers’ ability to embrace innovation at the core level. By integrating “run” and “grow” into a unified cycle, insurers can ensure that their technology investments yield long-term business growth. Collaboration with vendors who understand the entire spectrum of insurance operations is essential for realizing this vision.

The challenges posed by inflation, evolving risk dynamics, and new competition require insurers to adapt and innovate. By reimagining their approach to core systems and embracing a bundled strategy that unifies innovation, insurers can navigate disruptions effectively and thrive in an ever-changing landscape. The core is not just about maintenance; it’s the catalyst for driving innovation, differentiation, and sustainable growth.

Check out our CoreLeverage practice to see how you can build an adaptable, flexible, and growth-ready core with our accelerators and deep insurance expertise across the entire run, grow, and transform cycle.